Credit scores are a critical part of modern financial life. They influence whether you can get a loan, qualify for a credit card, or even rent an apartment. Despite their importance, many people don’t fully understand how credit scores are calculated or why they matter.

This article explains credit scores in a clear and simple way, breaking down the factors that affect them, common myths, and how to improve your score responsibly.

What a Credit Score Represents

A credit score is a numerical representation of a person’s creditworthiness. It summarizes financial behavior and predicts the likelihood of repaying debts on time.

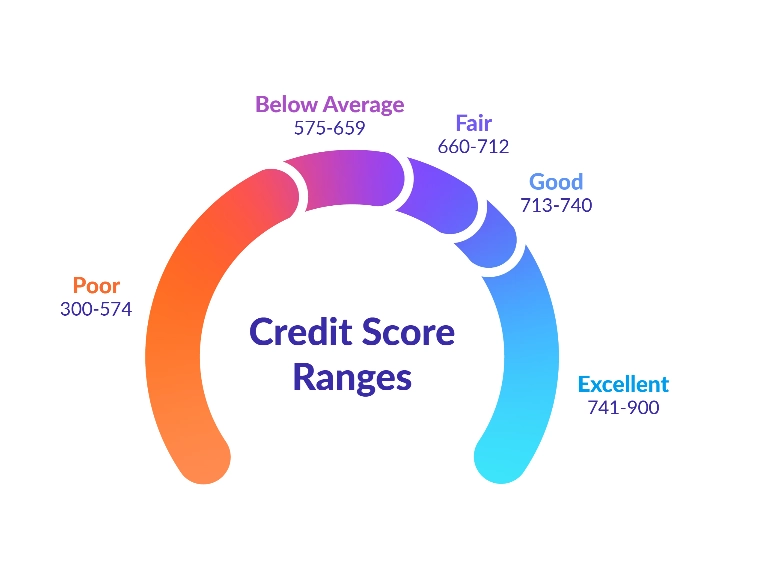

Scores typically range from 300 to 850, with higher scores indicating lower risk. Lenders use this number to determine interest rates, credit limits, and eligibility for financial products.

The Major Factors Affecting Credit Scores

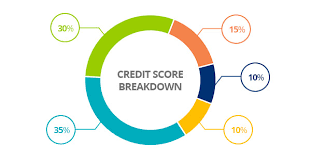

Credit scores are determined by several key factors. Each factor contributes a different percentage to the overall score:

-

Payment History (35%)

Timely payments on loans and credit cards are the most influential factor. Missed or late payments can significantly lower your score. -

Credit Utilization (30%)

This measures how much credit you use compared to your total available credit. Keeping utilization below 30% is generally recommended. -

Length of Credit History (15%)

Older accounts demonstrate experience managing credit responsibly. A longer credit history usually results in a higher score. -

Credit Mix (10%)

Having different types of credit, such as loans, credit cards, and mortgages, can positively impact your score if managed well. -

New Credit (10%)

Opening multiple new accounts in a short period can temporarily lower your score, as it may indicate financial stress.

Common Myths About Credit Scores

Many people misunderstand how credit scores work. Some common myths include:

-

Checking your own score lowers it – This is false. Personal inquiries do not affect your score.

-

Carrying a small balance improves your score – Not necessarily. Paying in full each month is often better.

-

Closing old accounts always helps – Closing long-standing accounts can actually reduce your score.

Knowing the truth helps you make better financial decisions.

How Lenders Use Credit Scores

Lenders use credit scores to:

-

Determine loan eligibility

-

Set interest rates and credit limits

-

Assess financial risk

A higher credit score often means lower interest rates and better loan terms. Conversely, lower scores may result in higher costs or denied applications.

Credit Reports vs. Credit Scores

While related, credit reports and credit scores are not the same.

-

Credit report: A detailed record of your credit history, including loans, payments, and inquiries.

-

Credit score: A numerical summary derived from the report, used for quick assessment by lenders.

Reviewing your credit report regularly is important to ensure accuracy and detect any errors or fraudulent activity.

How to Improve Your Credit Score

Improving your credit score takes time and consistent effort. Key strategies include:

-

Pay bills on time – Avoid late payments at all costs.

-

Reduce credit card balances – Lower utilization boosts your score.

-

Avoid unnecessary new accounts – Only apply when needed.

-

Maintain older accounts – Keep long-standing accounts open if possible.

-

Monitor your credit report – Correct any inaccuracies promptly.

Patience is essential. Scores rarely improve overnight but show significant gains over months of responsible behavior.

The Role of Credit Scores in Everyday Life

Beyond loans and credit cards, credit scores affect:

-

Renting apartments or homes

-

Obtaining insurance policies

-

Certain job applications

-

Utility deposits and mobile phone contracts

Maintaining a good credit score is not only about borrowing—it impacts multiple areas of financial life.

Common Pitfalls to Avoid

To protect your credit score:

-

Don’t miss payments

-

Avoid maxing out credit cards

-

Don’t apply for too much credit at once

-

Be cautious with co-signing loans

Being aware of these pitfalls helps maintain a healthy financial profile.

How Technology Helps Track Credit

Many apps and online services now allow users to monitor their credit scores for free. Real-time notifications and monthly updates help people stay on top of their financial health.

These tools make it easier to spot trends, understand credit behavior, and take action when necessary.

How Unpaid Debts Affect Credit Over Time

Unpaid debts don’t just impact your credit score immediately—they can have long-term effects. If credit card balances, personal loans, or other financial obligations remain unsettled, this information stays on your credit report for several years. Lenders use this data to evaluate risk, which means unpaid debts can make it harder to qualify for loans, credit cards, or even rental agreements in the future.

Small Loans and Credit Cards Build a Strong History

Managing small loans or credit cards responsibly is a smart way to strengthen your credit history. Paying off these accounts on time sends a positive signal to lenders that you handle credit reliably. Over time, this can improve your credit score and increase your chances of obtaining larger loans with better interest rates or higher credit limits.

Economic Trends and Market Competition Influence Scores

Economic conditions and competition between financial institutions can also indirectly affect your credit score. During periods of economic downturn or rising interest rates, access to credit can become limited, and some borrowers may take longer to repay debts. This behavior can influence scores even for otherwise responsible users. Staying aware of economic trends and planning finances carefully helps maintain a strong credit profile.

Final Thoughts

Credit scores are a numerical reflection of financial responsibility. By understanding the factors that influence them and adopting responsible financial habits, individuals can improve their creditworthiness and access better opportunities.